by Dr. Roland Amoussou-Guenou (Lawyer at the Paris Bar, Assistant Secretary of the Pan-African Council of the LCIA).

An Advisory Paper Presented by the International Law Firm SCP Weissberg

This paper was prepared for the Conference on the Arbitration of International Trade and

Investment Disputes in Africa held in Johannesburg, South Africa from 5-7 March 1997.

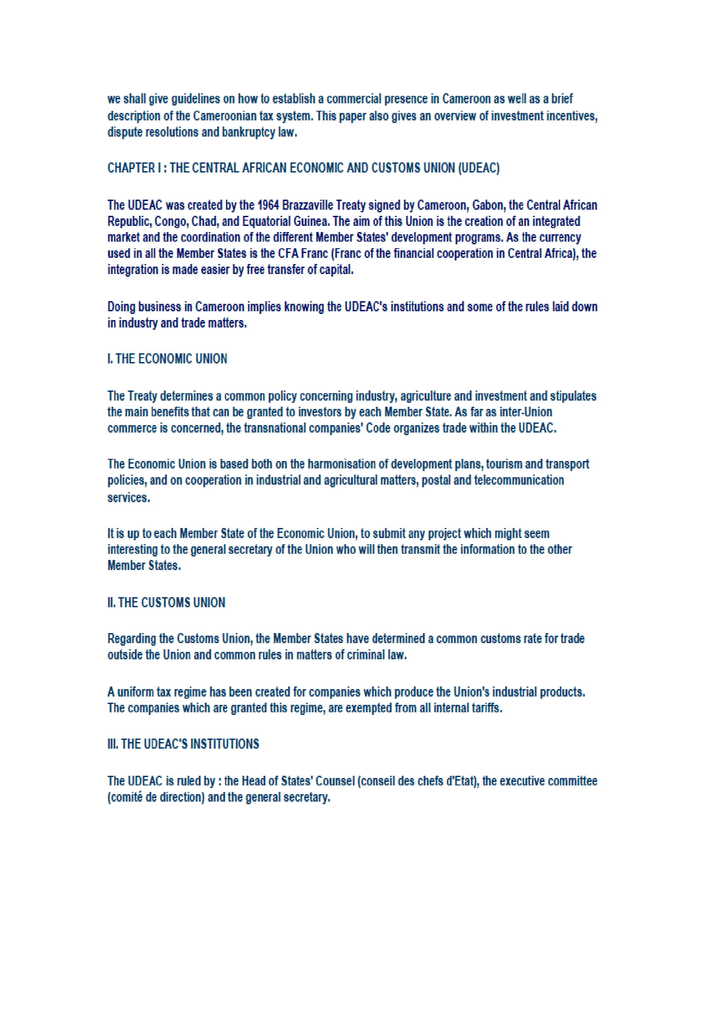

INTRODUCTION

A lot of preconceived ideas have been propagated concerning arbitration in Africa. Indeed, for

many practitioners and arbitrators from Western Countries, arbitration in this continent is

more or less, terra incognita.

It is true that while arbitration was developing and expanding fast all over the world, Africa

was being left behind in this race. In addition, the notable dearth of literature on arbitration in

this area cannot be denied (1).

Currently, significant steps are being taken regarding the laws and practice of arbitration in

Africa. On this basis, one must certainly admit that now the time is ripe for arbitration to

expand in this part of the world.

The purpose of this paper is to present the evolution of the arbitration laws and practices in

francophone Africa since anglophone Africa has already been very well covered (2).

African laws relating to arbitration included two main sets of rules. The first relates to the

general rules of law and the second to investment law. Both have domestic and international

sources.

Investment law contains a whole range of legal guarantees intended to attract investments. Included among these legal guarantees is arbitration. Thus "arbitration under the general rules of law" means arbitration not involving matters of investment law (3), which is itself an important but different issue that will not be considered here.

In order to locate ourselves within the evolution of arbitration under the "general rules of law"

in francophone Africa, it may be useful to consider the early sixties as the focal point.

The early sixties coincided with the accession to political independence of most of Africa's

sub- Saharan states. This time is also considered as the starting point of expansion of

international commercial arbitration (4).

I - The past: the background of francophone Africa's legal systems with regards to the

"Process of legislative extension"

This rule is particular to the French colonial system. It is established by the principle of

"Legislative specialty" (a), which needs to be illustrated here with some examples (b). After

which we will see that some of the difficulties with which francophone African countries have

been confronted to date, especially in the matter of arbitration legislation, originate from that

principle (c).

a) The definition of the principle "legislative specialty"

The principle of "legislative specialty" has a history that goes back a long way. Following

the Revolution of 1789, the French authorities established that "the status of the colonies are

determined by special orders ”(5).

From this time onwards, the laws applicable in France's overseas territories were those

enacted in the Metropole and extended to these territories by a special enactment of the

colonial legislator (6).

b) The application of the principle of "legislative specialty" in the matter of arbitration: some examples.

The impact of this principle in the matter of arbitration, can be examined in the light of the

Civil Procedure (i), the Commercial Law (ii) and the Administrative Law (iii).

i) The Civil Procedure

As far as arbitration was concerned, although the French Code of Civil Procedure was

extended to francophone Africa (7), surprisingly, the provisions related to arbitration in this

Code were not applicable.

This contrasts with the English African colonies, where the Arbitration Act of England was

deemed applicable (8). The example of Kenya is a good illustration of the difference between

the legal policies of the French and English colonial authorities.

As pointed out by Mr. Justice Coudrey OBE (9), the Order in Council of 1897 which established the Protectorate of Kenya provided that the Common Law, Doctrines of Equity, and Statutes of General Application in force in England on the 12th August 1897 should apply in Kenya (meant that from the beginning, The Arbitration Act of 1889 applied in this country).

This raises the important issue of why the French colonial authorities did not extend the

arbitration legislation to their colonies? Of course such a question is not easy to answer. One

acceptable hypothesis is that during the nineteenth century, arbitration as a judicial means of

settlement of disputes on the legal basis of the parties's agreement, did not fit in with the

French colonial policy known as "direct rule", as opposed to the "indirect rule" of the English

colonial system (10)

The French authorities were more dictatorial in administrating their territories. Their

preoccupation at that time was to keep tight control on the resolution of disputes in their

territories (11).

The lower judicial power was delegated to the indigenous authorities but at the same time,

any powers of arbitration which might interfere with the judicial organization mentioned

above were removed from the potential users of the Code of Civil Procedure (12).

Therefore, the absence of law concerning arbitration within the legal system of the French

colonies soon after independence originates from this French colonial policy.

ii) The Commercial Law

The French Code of Commerce was extended to the former French territories of Western

(FWA) in 1907 and Equatorial Africa (FEA) in 1910 13. Also applicable to the former

territories was the law of 31st December 1925 which completed the provisions of the Code of

Commerce and declares arbitration agreement valid in commercial matters (14).

It is noteworthy that this law of December 31st 1925, was enacted after the Geneva

Convention of 1923 on arbitration agreement (15), to which France was party in the context

of what may be considered as a certain "openness" to arbitration. This "openness", benefited

the French colonies because this law was declared applicable to them.

But paradoxically, this extension of the law of 31st December 1925 created an abnormal

situation in the legal sphere in that it produced the existence of a law admitting the validity of

arbitration agreements in commercial matters on the one hand, while on the other hand, the

rules of procedure enabling the arbitration process to work were absent.

iii) The Administrative Law

The Administrative Law represents one important particular of the French legal system

compared to the English Common Law. The French Administrative Law's prohibition of

arbitration as a means of settlement of disputes for administrative bodies was extended to the

colonies.

To the best of our knowledge, the only exception concerns Burkina Faso (ex Upper Volta),

where a law of 17th April 1906 authorizes arbitration for settlement of disputes in the matter

of public delivery or construction (16).

c) The limitations of "legislative specialty" with regards to the difficulties raised

The legislation in the Metropole was not extended systematically to all the territories.

Furthermore, when it occurred (which was not always the case as in the matter of arbitration

in the Code of Civil Procedure), the extension of the French law in the colonies, was only

effective from a precise date, sometimes after the original legislation was enacted. Thesis

extensions became the starting point of the evolution of the African legal system.

Any modification made in the law of the Metropole was only extended to the African law if

the modification was anticipated, which was rarely the case. This is the reason why African

countries lived, and are still living in a state of law that is out of date in the "exporting

country ”.

This situation added to the above mentioned legal vacuum in arbitration, results in a damaging

legal insecurity for business and trade transactions, which African judges and legislators are

trying to deal with.

II- The Present: current situation of arbitration laws in francophone Africa

The current state of arbitration of "general nature" (as opposed to arbitration of "investment

nature ”) concerns two main sources, domestic (a) and international (b).

a) Domestic sources of arbitration

Following independence in the 1960's, the majority of the new francophone African states

kept the status quo of their legal inheritance. As a result, no arbitration laws exist in their legal

systems to date (i). On the other hand, among the new African states which filled the vacuum

concerning arbitration legislation, some enacted laws related to domestic arbitration (ii) while

very few of them have promulgated laws on domestic and international arbitration (iii). In all

cases, arbitration laws in force in francophone Africa whether domestic or international, show

that "the basic connection with the parent legal system remains" (17).

(i) African states with no arbitration laws

These are Benin (18), Burkina Faso, Central African Republic, Gabon, Guinea, Mali,

Mauritania and Niger (19). The former French law on arbitration not having been extended

to these countries, means that there is a total legislative vacuum.

However, as already mentioned above, the Law of December 31st 1925 which authorizes

arbitration clauses in commercial matters is applicable.

(ii) African states with domestic arbitration laws

Contrary to what happened in the countries where the status quo was maintained, soon after

their independence, many French speaking countries enacted legislation related to domestic

arbitration. It would be interesting to review the situation in some of the countries concerned.

- Cameroon

The legal system of this country is influenced both by the French and the English law (20). Arbitration is governed by articles of the Code of Civil and Commercial Procedure (21) which are very close to the former French law on arbitration. It is to be noted that the previously mentioned law of 31st March 1925 is also applicable in Cameroon.

- Congo

The Code of Civil, Commercial, Administrative and Financial Procedure (22) of Congo

includes only one article governing arbitration. Indeed, under article 310 paragraph 2 of said

Code, a foreign award can be granted exequatur and enforced in Congo although the

arbitration agreement and the arbitral proceedings are not regulated.

One can deduce that there is a tacit acceptance of the arbitration agreement in the Congolese

law. Although it seems that Congo is not yet party to the New York Convention on recognition

and enforcement of foreign awards, one can conclude that the solution adopted by the

Congolese legislator is concise and effective as they have not thought it necessary to enact

other provisions to enable international arbitration.

The international validity of the arbitration agreement, derived from the well established

general legal principles of separability and competence-competence on the one hand, and the

domestic recognition of the foreign award on the other hand, seem sufficient to make

arbitration effective in the Congolese legal system.

- Senegal

This country was one of the most important territories in the French colonial policy in Sub-Saharan Africa (23). Arbitration is currently regulated in Senegal, in the Code of Civil Procedure promulgated in 1964 (24). These provisions are quite similar to those of Cameroon and therefore, to the former Code of Civil Procedure of France. The law of December 31st 1925 is still applicable in Senegal.

However a new arbitration bill has already been drafted and submitted to the legislative

authorities. This law will probably be enacted in 1998.

- Chad

In this country, arbitration is governed by Ordinance of 28th July 1967, related to the Code of Civil Procedure (25). It is influenced by former French arbitration rules, like the other former French colonies. One should bear in mind that the law of 31st December 1925 is also applicable there.

- Democratic Republic of Congo (Ex - Zaire)

Although it is a francophone country, the Democratic Republic of Congo (Ex Zaire), is not a typical French colony. This country was a former colony of Belgium, which is also a French speaking country. Arbitration is regulated in The Democratic Republic of Congo (26) by articles 159 to 194 of the judicial Code of 1960 (27).

(iii) African States with international arbitration laws

To date, only three countries are concerned: Djibouti, Ivory Coast and Togo (28).

- Djibouti

The Djiboutian Code of International Commercial arbitration which was the very first African legislation on the matter of international arbitration was enacted in 1984 (29).

It is influenced by the French decree of May 12th 1981 on international arbitration. Tea

definition of international commercial arbitration and the arbitral proceedings are organized

on the same legal basis. It is also in accordance with the modern instruments on international

arbitration such as the Geneva Convention of 1961 and the United Nation Commission for

International Trade Law (UNCITRAL) Model Law. It is important to note that The Federation

of the Chambers of Commerce of the member states of the Preferential Trade Area for

Eastern and Southern African States ("PTA") (30) decided in 1987 to create a Regional

Arbitration Center based in Djibouti. As a result, the Djiboutian Code may be of considerable

importance for arbitration in the region during the coming years.

- Ivory Coast

The Code of Civil, Commercial and Administrative Procedure of Ivory Coast of 1972 (31) does not regulate arbitration. Thus, when the tribunals of this country were to decide on the issue of the validity of the arbitration agreement, during the late eighties, they faced a serious obstacle. In the presence of contradictory decisions made by the lower courts, the chambers of the Supreme Court gathered to decide on the issue, which led to a decision of April 4th 1989 (32). According to this decision, the arbitration agreement is valid in Ivory Coast under the law of December 31st 1925.

In the light of the above the legislative authorities realized that the time had come to fill the

void in the area of arbitration in the country. This is why the law of August 9th 1993 related

to arbitration was passed.

The particular of this law is that it is nearly entirely based on the French decrees of 1980 on

domestic arbitration and 1981 on international arbitration (33).

- Togo

This country has two sets of rules related to arbitration. The first ones are subject to the decree of March 15th 1982 (34) also influenced by the former French Code of Civil Procedure.

The second are regulated by the law of 28th November 1989 which creates a Court of

International Arbitration on the model of the ICC Court of International Arbitration, in order

to promote international arbitration in Togo (35). To date, no records on arbitration

proceedings administered in Togo under the auspices of this Center have been brought to my

Warning.

b) International sources of arbitration

These concern both bilateral agreements (i) and multilateral conventions (ii).

(i) Bilateral agreements

Following the independence of the early sixties, France signed a great number of accords

with its forming colonies. They relate to co-operation in the field of justice and the enforcement

in one state of judgments handed down in another state. They also contain special provisions

regarding the recognition and enforcement of awards made in one country and "imported"

into the contracting country (36).

Although very useful in practice, these accords are not specific to arbitration, as they are

generally limited to reference to provisions of the New York Convention.

(ii) Multilateral conventions

It will be sufficient to mention The New York Convention of 10th June 1958 and the European

Convention on International Arbitration of April 21st 1961.

- The New York Convention of 10th June 1958

It has been notable success in Francophone Africa (37). As a consequence, the Geneva

protocols of September 24th 1923 and September 26th 1927, ratified by France and

applicable to its former colonies are now of limited interest.

- The Convention on International Arbitration of 21st April 1961

This Convention was drafted under the auspices of the United Nations Commission for

Europe and concerned European East-West trade. Hence, in principle, the African countries

are not covered. However, I should point out that Burkina Faso adhered to the Geneva

Convention on January 26th 1965 (38).

III - The future: The OHADA Treaty

As a consequence of what has been mentioned above, one can see that the laws in force in

Francophone Africa are not harmonized. This situation causes serious harm to regional

policies for trade and investment in the former French colonies (39).

Thus in 1963, the Ministers of Justice of the countries concerned aimed to harmonize the legal

systems they had inherited from the colonial period. This would make their legal systems

more coherent in order to facilitate their political and economic co-operation (40). Therefore,

in October 1992 in Libreville, (Gabon), the Heads of States of the Franc Zone approved the

project of a Treaty of Harmonization of Business Laws. On October 17th 1993, the draft

Treaty for Harmonization of Business Laws in Africa, was signed by fourteen member states,

and is already in force.

The Treaty is open to membership of other African countries and also to countries outside

Africa (41).

Article 3 of the Treaty creates an Organization for Harmonization of Business Laws so called

"OHADA", composed of a Counsel of Ministers and a "Joint Court of Justice and Arbitration"

(JCJA) which will be in charge of the realization of the goals of the Treaty. The legislative

texts, termed "Uniform Acts" (42), which will be directly applicable and mandatory in the

Member States "notwithstanding any prior or subsequent domestic provision", are the

principal means of realizing the objectives fixed in the Treaty.

The "OHADA" Treaty, attributes great importance to arbitration (43) and intends to set out

original rules in this matter. But to date, the "Uniform Act" on Arbitration has not yet been

drafted.

It seems important to emphasize the role of the JCJA (44) which has power of adjudication in

the issues of interpretation of the Treaty and also in judicial and arbitration matters.

Concerning this second power, the JCJA does not decide the dispute itself. It nominates or

confirms arbitrators, has an overview on the procedure and reviews the draft awards. Tea

JCJA also has power to grant exequatur to the final award.

In many aspects concerning arbitration, the organization and powers the JCJA seem similar to

the China International Economic and Trade Arbitration Commission or "CIETAC", under

the auspices of which “foreign-related” arbitration is administered in China since 1995 (45).

It is noteworthy that the major concern of the Draftsmen of the OHADA Treaty was to secure

the efficiency of arbitration agreements and awards. In this respect, they found unnecessary to

provide for grounds for vacating arbitral awards, contrary to widespread understanding

elsewhere (46).

This new African System is original and audacious in that it has restricted recourse to the

JCJA against an arbitral award only at the stage of recognition and enforcement.

CONCLUSION

As we can see, arbitration in Africa must not be considered as terra incognita, although

currently, international arbitration is only incorporated into the laws of three Francophone

countries and in the "OHADA" Treaty.

Two other countries, Benin and Senegal are preparing to enact new laws on domestic and

international arbitration.

However, in general, the legislations in force in the region have no "African distinctness".

They are very similar to the French system that they are based on, and The UNCITRAL

Model Law had no significant impact in francophone Africa, to date.

The expansion of international commercial arbitration in these countries will depend on the

enactment of modern legislations and the adhesion to the New York Convention of 1958.

In addition to this, the creation of efficient Arbitration Centers - the JCJA system still has to

prove itself - and the training of African lawyers must not be neglected.

Footnotes

1 See Tiewul SA and Tsegah F. “Arbitration and the settlement of commercial disputes: a

selective survey of African practice ”, The International and Comparative Law Quarterly, July

1975, p. 393.

2 See inter alia, papers presented by Judge Austin NE Amissah (Ghana), Prince Bola Ajibola

(Nigeria), Stephen Kokerai (Namibia / Botswana), Geoffrey WM Kiryabwire (Uganda), Prof

David Butler (South Africa), Ian Donovan (Zimbabwe) at the Resolution of Trade and

Investments Dispute conference held in Johannesburg from 5-7 March 1997. Adde

“Arbitration in Africa”, The LCIA and Kluwer Law International, 1996.

3 On the issue of arbitration involving matters of investment law, see Roland Amoussou-

Guenou "International Commercial Arbitration in Sub-Saharan Africa: Laws and Practice",

the ICC International Court of Arbitration Bulletin, Vol. 7/1 n ° 1, p. 63, and the footnotes…

4 See Bruno Oppetit “Philosophy of International Commercial Arbitration”, Journal Of

International Law (JDI) 1993, p. 811 and seq ...

5 See Claude Lussan, “Company legislation in the Overseas Territories and in the

associated territories (AOF - AEF - Madagascar - Togo - Cameroon), AIDE, Copyright

by Claude Lussan, 1953, pp. 20 & seq.

This principle was officially established by the Senatus-Consult (which is the denomination of

the decisions of the Senate under the first and second French Empire) of May 3rd 1854. See

also François Luchaire in the “Manuel de droit d'Outre-mer”, Paris, 1949. Adde “Quelle

are the laws automatically applicable? », D. 1950, Chr. p. 135.

6 For example, the Former Code of Civil procedure in force in France since 1807 was

extended to The West and Central African colonies by Decree of 15th May 1889 (see LA

1891, p. 39, J.CL Outre-mer, VI., Proc., Introduction). This rule has been reaffirmed by the

French Supreme Court. See Cass. Ch. Reunies 29th April 1959, Bull. civ. 1959, n ° 4p. 3 (PG

Yaoundé c / Fende); Bull. Civ. 1959, n ° 3, p. 2 (PG Yaoundé c / Malika).

7 See Decree of 15th May 1889.

8 See A. Allot, “Judicial and legal system in Africa”, London-Butterworths, 1962; J.

Vanderlinden, “African Legal Systems”, PUF, p.32.

9 Mr. Justice Coudrey OBE, “Arbitation in Kenya”, paper presented at the Inaugural

Conference of the Pan- African Council of the London Court of International Arbitration

(LCIA), Nairobi, Kenya, 7- 8th December 1994, p. 1.

10 See AJ Van Den Berg “Comparative study of commercial arbitration law

international in Common Law countries ”, Doctorate thesis in law, Aix, 1977. Adde T.

Hutchison “Africa and law. Developing legal systems in African Commonwealth nations ”,

Madison, University of Wisconsin Press, 1968.

11 See JP Musseron, “Power and justice in French-speaking Africa and Madagascar”,

Paris, Pedone 1966, pp. 23 & seq; Koffi Amega "Ten years of law in Africa", Penant 1972,

pp. 285 & seq.

12 See René Degni Segui “Codification and Unification of Law in Francophone Africa”, Rev.

Jur. and Pol. d 'Outre -mer, 1985, p. 285.

13 See decrees of 6th August 1907 and of 15th January 1910, “Legal Encyclopaedia of Black

Africa ”, Les Nouvelles Editions africaines; ISTRA, 1982, part I, legislation.

14 See Decree n ° 54-325 of 16th March 1954, Annotated collection of civil procedure texts and

commercial applicable in French West Africa by Gaston Jean Bouvenet, Paris,

ed. of the French Union, 1954.

15 See Lampue, “The application of the Treaties in overseas territories and departments”,

AFDI., 1960, p. 191.

16 See Alain Bockel “Administrative contracts: general data, the problem of

arbitration ”, Legal Encyclopedia of Africa, p. 265.

17 This expression also applies to the African countries of English influence. See A. Allot,

“Judicial and legal system in Africa”, op. cit, p. 54.

18 Information from Benin indicates that the Beninese authorities are preparing to pass a

domestic and international arbitration bill.

19 For more details on these countries, see Roland Amoussou-Guenou the ICC International

Court of Arbitration Bulletin, op. cit p. 64.

20 See Wendy Dorman, “Cameroon”, World Arbitration Reporter Issue 0 (1986) p. 1081.

21 See articles 576 to 601 (Book II part II)

22 Law n ° 51/83 of 21st April 1983

23 Dakar was the capital of the French empire in Black Africa.

24 See Book III, title I (arbitrations), articles 795 to 820

25 See articles 370 to 383

26 See articles 159 to 194.

27 See Decree of March 7th 1960, updated on July 30th 1985.

28 Draft arbitration Bills are currently being prepared in Benin and Senegal.

29 See Law of 13 February 1984, Rev. arb. 1984, p. 533 & seq. commented by Yves Derains.

30 The PTA was created on 21st December 1981 and came into force on September 30th

1982.

31 See Law n ° 72 833 of 21st December 1972, Official Gazette (JORCI) of 5 February

1973.

32 See Talal Massi v / Omais, April 4th 1989, Rev. arb. 1989, p. 530, commented on by

Laurence Idot

33 Law n ° 93-671, Official Gazette (JORCI) of September 14th 1993.

34 See articles 275 to 290 of the Code of Civil Procedure.

35 See Law n ° 89-31 of November 28th 1989, instituting an Arbitration Court (JORT of

January 10th 1990).

36 See Ministry of Foreign Affairs, “List of Treaties and Agreements of France in Force…. ",

Directorate of Archives and Documentation, Conservation of Treaties.

37 See List of contracting states, Multilateral Treaties, UN Secretariat General, vol 330, p.3

38 Cf. list of signatory states, Multilateral Treaties, UN S ecretariat General, doc. I UN XX

557, p. 744.

39 See Akimuni, AM, “A plea for harmonization of African investment laws”, African Law

Journal 1975, p. 134 & seq.

40 See Mr President Keba Mbaye, in “Harmonization of Business law in the Franc Zone“. Year

experience of judicial integration in Africa. Bulletin of the International Institute of Law

of French Expression and Inspiration.

41 See article 53 of the Treaty.

42 See article 5 of the Treaty.

43 See articles 21 to 26.

44 See Aboubacar Fall, “Harmonization of Commercial Law in the Franc Zone”,

International Business Lawyer, February 1995, vol. 23 n ° 2 p. 82; Pascal Agboyibor «Recent

Developments in the Planned Harmonization of Business Law in Africa ”, International

Business Law Journal, 1996, n ° 3, p. 30 ; Roland Amoussou- Guenou «Arbitration Pursuant

to the Treaty For Harmonization For African Business Law ”, International Business Law

Journal, 1996, n ° 3, p.321.

45 See Sally A. Harpole, “International Arbitration in the People's Republic of China under

the New Arbitratin Law ”, The ICC International Court of Arbitration Bulletin, Vol. 6 / N ° 1,

May 1995, p. 19.

46 See inter alia sections 66 and 67 of England Arbitration Act 1996, article 1504 of the

French New Code of Civil Procedure, article 34 of the UNCITRAL Model Law.