Legal aspects of setting up French companies abroad: the example of the United States (Fr)

"The life and blood of international commerce" (1) is the term used by English courts to characterize documentary credit.

Documentary credit can be defined as "the operation by which a banker, intervening on the order of a buyer for the financial settlement of a commercial transaction, most often international, promises to pay the seller against delivery of documents" (2).

According to Dean Jean Stoufflet, the documentary credit technique is "the greatest success of international trade in terms of banking mechanism" (3).

Other authors have called it "a true masterpiece of banking technique" (4).

Indeed, in international affairs, due to the geographic distance of the contracting parties who often do not know each other and it is difficult for them to trust the first operation.

The exporter is hesitant to undertake the manufacture or delivery of a product if he is not sure of being paid. For its part, the importer is reluctant to pay funds to the exporter before being sure that the shipment has been completed within the prescribed time.

Documentary credit, by involving the independent and solvent intermediaries that are the banks, therefore constitutes a means of payment which has the advantage of reconciling the divergent interests of the buyer and the seller.

The seller is guaranteed to receive against delivery of certain documents, the price due to him due to the delivery of the goods within the agreed time.

The buyer, on the other hand, will only have to pay for the goods ordered if it has actually been sent to him.

As such, it can be considered that documentary credit is an instrument of confidence based on the international banking system.

Thus the myriad of commercial transactions and the development of international exchanges make documentary credit one of the most important instruments of international trade.

Consequently, the monumental development of international trade in China is necessarily accompanied by the development of documentary credit, we can even say that in China the use of documentary credit is an essential operation for carrying out commercial transactions with foreign partners. .

In the international business community, documentary credit has been the subject of

regulations issued by the International Chamber of Commerce (ICC), organization

international private sector which has developed uniform rules applicable by traders

coming from very different economic and legal systems. The effectiveness of these rules has been

demonstrated by practice and sanctioned by case law. These "Rules and Practices

Uniforms relating to Documentary Credits' (UCP) were published for the first time

in 19335. Regularly revised to monitor and support changes in practice,

their latest version the "RUU 600" replacing the previous version the RUU 500 dating

of 1993 entered into force on July 1, 2007. The UK as lex mercatoria receives

consequently its full application in China by recognizing the right of the parties to

choose the rule of law applicable in international transactions involving the use

documentary credit.

On the other hand, at the national level, it did not exist 4 years ago in China, as in many

other countries, including France, no legal or regulatory provision governing credit

documentary. Chinese state law which is intended to apply to supplement the

possible shortcomings of the UCP is constituted by the provisions contained in the Law on

General Principles of Civil Law, the Law on Contracts, the Law of Security Interests and the Law of

Civil Procedure. However, due to the fact that these provisions are generally very vague and are

therefore open to interpretation by the judge, and that case law is not a real

source of law in China, since 1995, disputes over documentary credits have been

extensively brought before the People's Court of China.

Until 2004, the Supreme Court of China has ruled on more than 100 cases, without

count hundreds of questions relating to documentary credits posed to the Court

Supreme by the lower courts. Thus, China Banking Regulatory Commission, banks

sales representatives also asked questions about the enforcement of court judgments

concerning documentary credits, given that legal explanations or

regulations emanating from the Supreme Court constitute one of the most important sources of law.

important in the Chinese legal system.

Having regard to these various questions raised in practice, particularly with regard to the law applicable to documentary credit, the criterion of document verification, fraud etc., the Supreme Court of China, after having made a global study and discussions with lawyers, practitioners, banks and CCI experts in China, drawing inspiration from the RUU500, adopted on October 24, 2005 the Rules of the Supreme Court on some questions concerning credit disputes documentary, which entered into force on January 1, 2006. Although the general provisions provided for in the aforementioned laws are still applicable, the Regulations provide judges and thus practitioners with more accuracy and precision in the event of diverging interpretations and also completes gaps under the UCP. However, this Regulation is not without faults, especially since the entry into force of RUU 600.

Regarding the scope of the Rules of the Supreme Court on some issues

concerning disputes relating to documentary credit, its first article provides that the

Rules apply to disputes relating to the issue, notification, modification,

revocation, negotiation and lifting of documentary credit. Here, the word "revocation"

means the application of the Regulations to revocable documentary credits. Expression

revocable credit means the documentary credit that can be amended or canceled by the bank

Issuer at any time and without agreement or information from the beneficiary 6.

However, in practice, revocable credits have disappeared for several years. Pulling

the lessons of this development, the UCP 600 no longer refer to the concept of credit

revocable. Drawn up under the control of UCP 500, the Regulation did not take into account this

evolution, which on the other hand gives the issuing or confirming bank the possibility

to attach the irrevocability of their commitment to pay conditions calling into question

the very principle of this commitment. These so-called "soft clauses" would have

consequence of making revocable documentary credits and therefore considerably harms

the interest of the beneficiary. Indeed, only the irrevocable credit is a real guarantee for the

beneficiary insofar as this type of credit constitutes a firm commitment by the banker

transmitter. The revocability of the documentary credit is contrary to the very principle of this

guarantee, consequently it would be preferable for the Regulation to delete in its field

the revocation of the documentary credit to be compatible with UCP 600 and

truly reflect business practice.

This article is limited to presenting two essential points of the documentary credit provided

by the Regulation which in practice give rise to more problems, namely the verification of

documents (I), and documentary credit fraud (II), as well as some thoughts on these

points under the rules of RUU600.

Document verification is an essential mission of the banker in the context of a documentary credit. As Mr. Affaki notes, "in an operation which is marked by the separation between the underlying commercial contract and the banking intervention, the outcome of this intervention is exclusively a function of documents and not of the realization of facts which may be reflected there ”(7). It is an important and growing source of litigation in the practice of documentary credit. This situation obviously affected the safety of the technique. It appeared that more than 70 % of the first presentations were irregular. Most of the difficulties relate to issues of document compliance. It is therefore one of the objects of the Regulation to minimize the risk of rejection for irregularity of documents.

Section 5 of the Regulations provides that the issuing bank is required to honor its commitment to documentary credit when the documents presented are apparently in conformity with the terms of the credit, and all documents are apparently compatible with each other. It appears that the criterion of document verification in China is the criterion of strict compliance of documents with the stipulations of documentary credit. It is obvious that the banker cannot know all the commercial uses and consequently the beneficiary cannot ask him to consider as conforming documents which are not strictly identical to the stipulations of the credit.

Thus a bank does not have to interpret the description of a commodity, even when the

terms used in documents separate from those of the credit, for professionals of the

strictly equivalent trade. In a judgment of the Guansu Court of Appeal on June 25, 2007,

the Court supported the refusal of payment by the confirming bank, considering that the name

of the goods "grapes" stipulating on the invoice does not correspond to the name "dried

currents ”appearing in the documentary credit, although in international trade this

or almost the same goods. It should therefore be noted that the criterion of conformity

substantive was not upheld by the Chinese People's Court, which is contrary to the

jurisprudence of certain countries and in particular of the United States. Consequently, article 5 of

Regulation limits the obligation of the banker to a control of appearance of presentation

compliant. This is a protective rule for the banker in charge of verification who does not

benefit the recipient.

However, the principle of strict compliance has been strongly weakened by the Regulation, which

is also the case law trend, since Article 6 paragraph 2 specifies that in the case of

where the apparent conformity of the documents with the credit stipulations and the

inter-documentary compatibility are not strictly satisfied, since there is no

ambiguity or contradiction between them, the People's Court may consider that the

documents are compliant. Thus the Shanghai Court of Appeal overturned a decision having

excluded the responsibility of an issuing bank towards the beneficiary by qualifying as

a "purely formal" divergence which did not create any ambiguity in the fact that on a

transport document, the names of the recipient of the goods and the one to receive

notification of the arrival of this commodity, appeared in the wrong boxes and did not

not corresponding to the stipulation of the documentary credit.

From this point of view, the Regulation tries to maintain the balance between the interests of the banker

and the beneficiary while preserving the principle of strict compliance of documents by

in relation to the credit stipulations. Nevertheless, provisions of the Regulations drafted

very generally are susceptible to different interpretations, especially in relation to

RUU600 which provides detailed provisions by different types of documents. In

Consequently, these provisions do not give clear answers helping the courts to

rule.

The regularization of rejected documents is always possible as long as the credit is not

expired and that the irregularities are subject to correction. On the other hand, when the

regularization of documents is not possible, Article 7 of the Regulations authorizes the bank

issuer, at its sole discretion, to request the agreement of the ordering party to accept

irregular documents.

However, the authorization to lift irregular documents given by the client

does not oblige the issuing banker to pay the loan to the beneficiary. When the transmitter has

refused the lifting of irregular documents, the payment request of the beneficiary who

prevails of the acceptance of irregularities by the principal, must be rejected by the court.

This is contrary to French case law, since in a judgment of March 11, 2003, the Paris Court of Appeal decided that the bank was obliged to pay in circumstances where the originator, meanwhile declared in receivership , had agreed to the payment of irregular documents. However, it should be remembered that the bank has no obligation to request from the originator any possible lifting of irregular documents even if the latter, without being questioned by the bank, intends to accept the documents. The formality of the documentary credit authorizes the banker, whatever the position of the principal on the execution of the basic contract, to refuse to honor his commitment since the documents presented in support of the request are not strictly meet the specifications of the letter of credit 8.

However, some Chinese lawyers consider that this article, authorizing the banker to refuse

irregular documents, even with the agreement of the principal, resulting in

to the interests of the principal and the beneficiary, and considerably increase the cost of

international transactions with full emphasis on the principle of credit autonomy

documentary. This article does not take into account the purpose of document credit, which is to ensure the

payment of the commercial transaction of which the good progress and the good result, goal

pursued by the parties, namely the ordering party and the beneficiary of the documentary credit.

Fraud is the only exception that can hinder the free play of documentary credit mechanisms. In particular, it hinders the payment of documents which appear to be regular (9). Although the maxim fraus omnia corrumpit is generally accepted by all legal systems, in the area of documentary credit, the qualification of fraud and its taking into account are highly variable (10). Given the differences in fraud between the different legal systems, the RUU600 deliberately leaves the problem to national law.

On this issue which generates as much difficulty as the verification of documents

in practice both for the banker and for the Court, the Regulation therefore clarifies the

qualification of documentary credit fraud and its effect on bankers, the

principal and beneficiary. However, this qualification is questionable, according to many

lawyers and practitioners, because its scope considered too broad.

Article 8 provides that fraud is established when the beneficiary:

Under this article, it is interesting to note that by listing the cases of fraud, it does not give its definition or characteristics, which suggests that the article applies to all frauds. provided for in these four cases, contrary to American or French case law which requires that fraud be substantial or manifest.

This would have the effect of widening the scope of the fraud exception principle and

lead to even more refusal of payment by the banker who could easily invoke

fraud, and consequently compromise the efficiency and speed of documentary credit.

Regarding the first and third scenario, that is to say the beneficiary infringed or

falsified documents or presented documents that he knew were false as soon as

the origin; and the beneficiary, with the collusion of the principal or a third party, presenting

false documents without any real transaction, we can see that these are the most

more common in practice, and relatively easy to establish.

However, what raises the most problem is the second scenario in which the

beneficiary in bad faith does not deliver the goods or delivers the goods

devoid of any value. Here, the border between the poor execution of a contract

commercial and fraud could raise difficulties of appreciation. A fortiori, the

bad faith on the part of the beneficiary is sometimes difficult to demonstrate. In a judgment of the Court of Appeal

of Tianjing on November 28, 2006, the Court found the issuing bank liable

citing fraud in the circumstances in which the seller issued, instead of a certain

dry medicinal plant, the fresh medicinal plant which has rotten during transport from

China in Korea, on the grounds that the fresh plant fully met the stipulation of

documentary credit that did not specify the condition should be this plant.

It should be noted, however, that in this case, the bad faith of the seller could have been

established from the fact that the fresh plant has practically no medicinal effect, and the

recipient should have anticipated the possible rotting during the long transport.

As for the last paragraph, it groups together all the other frauds not provided for by the

three cases, which leaves a wide margin of appreciation to the courts. It shows

that the acts which could be qualified as fraud do not appear to be clearly defined by the

Regulation and therefore the application of the fraud exception principle raises

often many difficulties, legal uncertainty remaining.

Article 9 of the Regulations provides that the fraud provided for in Article 8 authorizes bankers

and the principal to request the Court to suspend payment of the credit

documentary. Thus, it deprives the beneficiary of his rights under the documentary credit and

exonerates the responsibility of the banker, whether it is an issuing bank,

confirming, nominated or negotiator.

Article 10 also specifies that once fraud has been noted by the Court, it must order the suspension or cessation of payment of the documentary credit, except in the following cases when:

It is therefore considered that the issuing or confirming banker is required to reimburse the bank

intermediary authorized to carry out the documentary credit if this bank has regularly

carried out, before the discovery of the fraud, the credit in view of apparently compliant documents

the stipulations of the documentary credit.

The fraud therefore opens recourse to the banker who paid the documentary credit and

this, even if the banker committed a fault in the verification of the documents and paid the

documentary credit without any reserve since it has not discovered the fraud before

payment and was thus in good faith. However, what is very regrettable is that the text does not

not provide for the cases of documentary credits payable in the future where the intermediary bank

had paid the beneficiary in advance of the date agreed for the completion of the

documentary credit. It should therefore be added to this text that the banker who anticipates the

realization of the documentary credit does so at its own risk.

In the same vein, the principal will have to reimburse the issuing banker who has

lifted "false" documents when there was nothing to suspect their authenticity. Se

asks the question of knowing when the principal is availing himself of a fraud affecting the

documents of a documentary credit in order to paralyze the payment by the bank:

does the bank have an obligation to refuse payment? The Rules do not give us an answer,

court decisions are divided on this point.

***

The Rules of the Supreme Court on certain questions concerning disputes relating to the

documentary credit undoubtedly provides the courts with more precision and certainty

to rule on disputes relating to documentary credits. Nevertheless, we must admit

that it is far from complete and that the UCP in its current version still remains a source

very important law for Chinese courts, and important case law

foreigners also have considerable influence.

(1) Harbottle RD (Mercantile) Ltd. V. National Westminster Bank Ltd., (1978) QB 146, (1977), 2 All. ER862.3 WLR752.

(2) Ch. Gavalda and J. Stoufflet, Banking law: Litec 2005, 6th ed., P. 403.

(3) J. Stoufflet, Documentary credit: Litec 1957.

(4) J.-P. Mattout, International banking law: Bank 2004, 3rd ed., P. 259.

(5) J. Stoufflet, The normative work of the International Chamber of Commerce in the banking field, in Studies offered to Berthold Goldman: Litec, 1987, p. 364 and s.

(6) RUU 500, art. 8

(7) G. Affaki, op. cit., n ° 139.

(8) G. Affaki and J. Stoufflet: Banque et Droit, 2004, n ° 95, P62, obs.

(9) Cass.com. March 4, 1953, S. 1954-1-121, Lescot note

(10) M. Vasseur, notes Cass.com. April 7, 1987, DS 1987, p399

Kenneth WEISSBERG, Lawyer at the Court of Paris; with the support of Xing HU, Graduated from Xiamen University (China) and Paris X and Paris II Universities

After more than thirty years of preparation, the project of a European Company (SE) has finally seen the light of day thanks to two texts, namely Regulation (EC) n ° 2157/2001 relating to the statute of the European Company (ci¬ after the "Regulation") as well as Directive 2001/86 / EC supplementing the statute of the European Company with regard to the involvement of workers (hereinafter the "Directive"), both dating from October 8, 2001.

The Regulation entered into force on October 8, 2004, and the Member States of the European Union should have adopted on that date the laws, regulations and administrative provisions necessary to comply with the Directive, these two inseparable texts being called upon to apply concomitantly.

The very ambitious project at the outset, aimed at harmonizing national laws and creating standards for a new uniform type of society, was successively abandoned because of too great differences between the legal systems of the member states.

What is it really ? What is the point of this new legal form? How will it be implemented?

The Regulation establishing the statute of the SE comes down to a new and optional legal formula which is closely, but with a certain flexibility, based on the rules already applicable, in each Member State, to public limited companies.

As a result, the SE provides a framework that can be adapted conventionally and on which the standards of the twenty-five legal systems of the member states can play.

Consequently, if the SE is of Community law, it is the law of the State where its head office is located and its central administration (corresponding to the effective and actual seat of the management) which will apply in all areas not governed by the Regulation, the Directive or its statutes.

This local law will in particular be decisive for all the terms of the constitution. At present, the vast majority of legal literature seems to rule out the possibility of constituting an “ex nihilo” SE by investors subscribing directly to its capital. There remain therefore the following four modes of constitution:

(a) incorporation by merger, reserved for public limited companies from different Member States,

(b) the creation by creation of a holding company, open to public limited companies and limited liability companies having a community presence through its subsidiaries or branches,

(c) incorporation in the form of a joint subsidiary, reserved for public or private law entities if two of them are governed by the law of different Member States or have had, for at least two years, a subsidiary or a simple establishment falling under the law of another member state,

(d) by conversion of a public limited company into an SE, provided that the latter has a subsidiary in another Member State.

Any constitution requires the drafting of the statutes, including the necessary mentions in any public limited company of the Member State in which the SE will have its statutory seat and its central administration, and a share capital of a minimum amount of 120,000 euros.

Thus, it would be possible to have an SE registered in France using public savings with a share capital of only € 120,000, while the minimum provided for in the Commercial Code for public limited companies in this case is € 225,000 . The statutes freely decide whether the SE will have a board or dualist system, the State not being able to impose its system. It is likely that when employee representatives are called upon to sit on management or executive bodies, it will be easier to opt for a dualist system, letting them enter the Supervisory Board rather than the Board of Directors.

In addition, the freedom of freedom of the editors is the same as that for the establishment of the statutes of an ordinary limited company having its seat in the Member State concerned. It should be noted that considerable differences exist in this respect between the various member states (the United Kingdom and Ireland, for example, leaving a great deal of contractual freedom, while there are other states, such as Germany leaving. the principle that "anything that is not expressly authorized is prohibited").

Except in the case of the establishment of a subsidiary in the form of an SE, registration according to the legislation of the Member State where the statutory seat is located, which marks the starting point of the legal personality of the SE, must be be preceded by negotiations with the employee representatives of the companies concerned regarding their involvement, namely their information, their consultation, or even their participation in the management or executive bodies of the company, the aim being to preserve the rights acquired before the Constitution.

In this regard, as soon as possible after publication of the draft constitution, negotiations must be initiated within a "Special Negotiation Group" (GSN), specially formed for this purpose according to the rules provided for in the Directive, ensuring it proportional representation of the number of employees concerned in each member state. Many details regarding the methods of appointment of its members, their status will be regulated by national law, in other words the laws transposing the Directive.

Three possibilities open up, depending on the outcome of these negotiations:

• either the GSN reaches an agreement,

• or it has decided (with a qualified majority of 2/3 of its members, representing at least 2/3 of the workers, this figure including the votes of members representing workers employed in at least two member states) not to begin negotiations on this point or to close open negotiations and to apply the information and consultation regulations applicable in each Member State where the SE employs employees,

• or finally at the end of the six-month negotiation period provided for by the Directive, extendable for an equivalent period, no agreement could be concluded.

In the latter case only, the reference provisions provided for by the Directive will imperatively apply as soon as the registration of the SE is implemented.

On the other hand, if the SE is incorporated by transformation, these provisions only apply if the rules of a member state relating to the participation of workers in the administrative or supervisory body were already in force in the transformed company. in SE.

In the other three hypotheses of incorporation, these rules only play if, before the registration of the SE, one or more forms of participation applied in one or more companies having directly participated in the operation by covering at least 25 % the total number of employees for all of these (50 % in the case of a SE holding company or subsidiary); if the total number of staff remains below these thresholds, a decision by the SNB is required to make the reference provisions of the Directive applicable.

a) Consultative body

At a minimum, these reference provisions provide for the creation of a single "consultation" body in the Member State where the future SE is registered and in which the employee representatives are expected to sit alone. Its members are elected or appointed (according to the rules laid down in the transposition law of the Member State where the SE is registered) in proportion to the number of workers employed by the participating companies, their subsidiaries or establishments concerned. Each state is allocated one seat per tranche of workers employed there representing 10 % of the number of workers employed in all the States of the Union or a fraction of the said tranche.

The consultative body has the right to meet the competent SE body (board of directors, executive board) at least once a year, on the basis of regular reports drawn up by the latter, in order to be informed and consulted about the development of the SE's activities and its prospects.

These meetings relate in particular to the structure, the economic and financial situation, the probable development of activities, production and sales, the situation and probable development of employment, investments, substantial changes concerning the organization , the introduction of new working methods or new production processes, production transfers, mergers, capacity reductions or closings of companies, establishments or significant parts thereof and collective redundancies .

In addition, when exceptional circumstances occur which considerably affect the interests of the employees, in particular in the event of relocation, transfers, closure of companies or establishments or collective redundancies, the advisory body has the right to be informed and meet with the management body of the SE, without having a right of veto and having an obligation of confidentiality.

In summary, the functions and powers of this consultative body do not differ much from those which French law recognizes for works councils.

b) Employee participation in administrative or supervisory bodies

The situation is different for workers' participation, a true German "cultural exception", but which is therefore only essential if there is an involvement of a German company in which the rules of "Mitbestimmung" (co- management) were already applicable before the registration of the resulting SE (mainly public limited companies under German law with more than 500 employees).

If none of the participating companies was governed by participation rules before the SE was registered, it is not obliged to introduce provisions on employee participation.

Ultimately, it can be noted that in many cases, the SE can be set up without employee participation in the SE's administrative or supervisory bodies. In fact, the agreement to be reached does not necessarily have the objective of setting up employee participation, and the Community system leaves companies considerable room for maneuver in this regard, however at the cost of complex regulations.

a) Cross-border mergers

The main assets lent to the SE are its mobility within the European Union. Its registered office can be transferred while maintaining the legal personality of the company. Its adoption could allow a simplification of the administrative structures of the companies and would contribute to a reduction in costs.

For France, the main interest is probably that the Regulation provides a mechanism for cross-border mergers, an operation which French law does not prohibit, but which it has so far ignored.

The Regulation provides a framework that would allow two entities to be merged quite easily even outside of a mother-daughter context. However, due to the numerus clausus of eligible legal forms (in particular the Simplified Joint Stock Company is not one of them!), The operation may require prior transformation.

b) "Forum shopping"

As it stands, the legal form of the SE looks more like a building site than a “finished product”. In order to finally allow its adoption, it was deliberately omitted to make specific provisions in the fields of taxation, competition, intellectual property or insolvency.

In the absence of Community harmonization, it is therefore the law of the Member State in which the SE has its seat which is intended to be applied and which may be more or less restrictive.

The choice of the state of establishment therefore deserves in-depth research in relation to the legal, social and fiscal environment of the countries likely to host the SE, in order to be able to take advantage of the opportunities offered by the significant differences remaining between the European Union member states in this regard.

This kind of “forum shopping” is regularly out of reach for companies that are not already real European players and used to handling different legal systems.

Others will quickly discover the attractions of the United Kingdom and Ireland for their great flexibility in terms of company law rules, the low cost of registration and their low corporate tax rate and Spain for its quasi - absence of rules imposing an implication of the employees in the business of the company. On the other hand, Germany, with its compulsory co-management, the main reason for the low strike rate in the country, risks appearing complex for foreign investors. Example: the Airbus group, which one might think is predestined to organize itself in the form of an SE and currently in the reorganization phase, declared that it was not interested in this legal form due to social constraints, given the large number of employees the group has in Germany.

Legal and tax competition between member states to attract investors is fully underway. There are sites on the Internet that offer Spanish or English "ready to use" shells. The reaction was immediate: at one of the last summits, the governments of France and Germany called for an acceleration of the harmonization of tax law at Community level to counter the dumping effects .

In this sense, the SE is a perfect example of the dynamics specific to most Community texts, also called the spill over effect: the gaps left by the Member States during the adoption will be satisfied, by other texts or the jurisprudence of the European Court of Justice interpreting the texts using the famous "useful effect".

France has not yet transposed the Directive.

Two draft laws have been drawn up so far: the Marini project, which confines itself to adjusting company law, in order to better integrate the new legal form of the SE and to increase the competitiveness of SEs registered in France, and the project presented by Senators Branger and Hyest, which includes the social aspect, in other words the transposition of the Directive.

a) The Marini project

An essential point of Senator Marini's project is to want to give SEs that do not make public savings flexibility in the arrangement of relations between shareholders comparable to that existing in France for SAS.

In addition, the project aims to abolish the provisions of the Commercial Code imposing a minimum number of shareholders in public limited companies and the need for directors or members of the supervisory board of a public limited company to have the status of shareholder , thus allowing the creation of a one-person SA.

b) The Branger / Hyest project

Senators Branger and Hyest also wish to make public limited companies more attractive by proposing the creation of a "simplified public company" with the aim of providing a "bridge" between the SA and the SAS, by a streamlined transformation procedure allowing SAS, when its statutes are compatible with French rules resulting from the transposition of Community directives applicable to public limited companies, to be considered, by means of a declaration of conformity, as a simplified form of SA. They will thus be able to take the name of simplified public limited company without questioning its statutes while avoiding the constraints linked to the transformation into public limited companies.

With regard to the transposition of the Directive, the project proposes to integrate a Title IX in Book IV of the Labor Code, entitled "On the involvement of employees in matters relating to European society". Its provisions transpose the Directive and exercise the options contained therein to comply with the employee involvement system in force.

Unfortunate tendency of the current legislation in France, the project leaves a good number of points to regulate by the government by way of decree, which makes illusory that in the next time, an SE could be registered in France.

The two projects not being very far apart from each other as regards the measures envisaged for the adjustment of company law, and the project for the transposition of the Directive remaining unsurprising, it is quite likely that the end result will be a combination of the two.

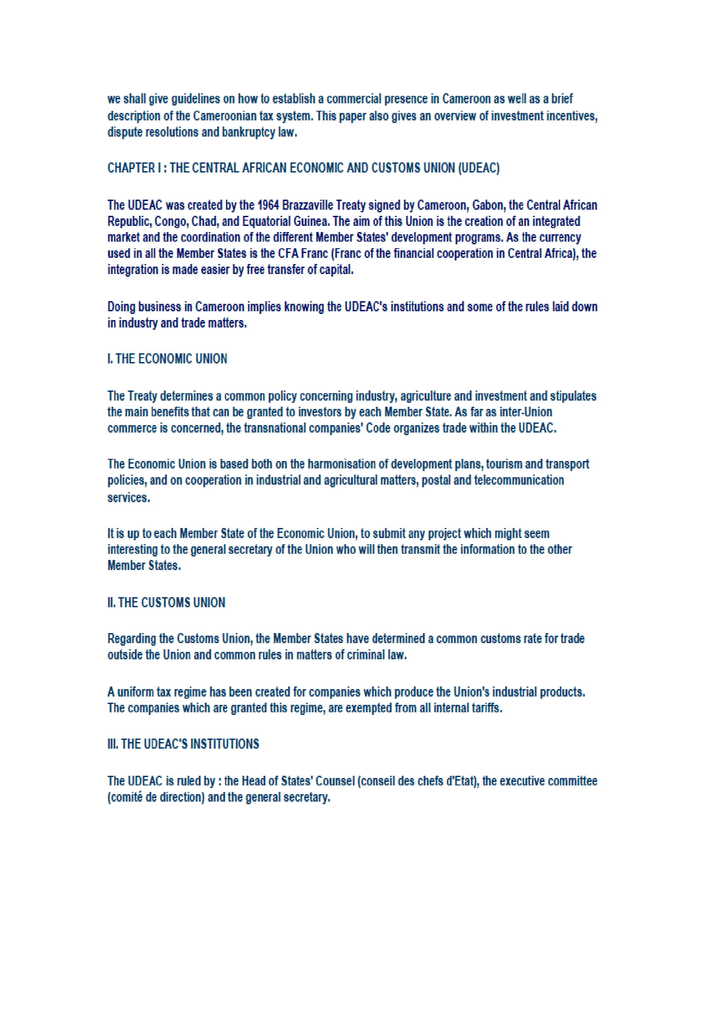

A guide for business in Cameroon: Cameroon is a developing country located in Central Africa in which investment is considered as being the active seed which generates growth and development.